INDIANAPOLIS – The laundromat industry is being flooded with sales pitches about “cashless convenience” and the supposed death of coin-operated stores. Card-system providers promise higher revenue, less theft, easier management, and a more modern customer experience.

And to be fair, there are advantages to accepting credit/debit cards in a laundromat.

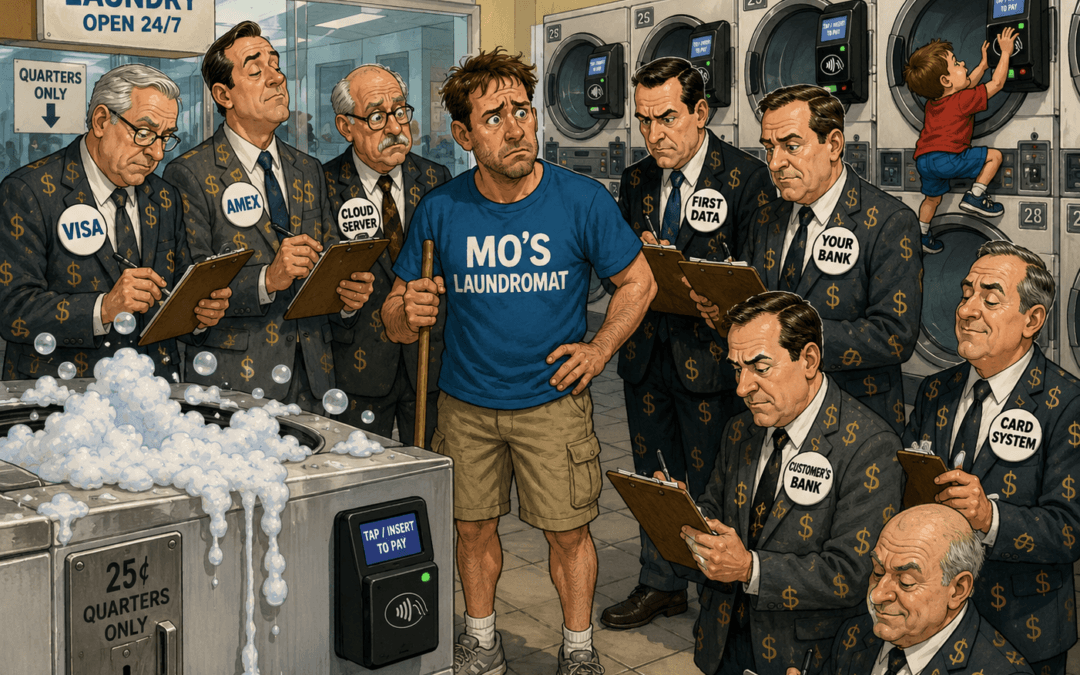

But many owners are beginning to realize there’s a difference between accepting cards and becoming completely dependent on a digital payment ecosystem.

Most card payment providers focus on the approximate 3.5% to 4.25% transaction fees. What they don’t emphasize are the additional monthly costs: service fees, server fees, compliance fees, gateway fees, maintenance fees, and support fees. Each system has a different way of getting there, but they all get there. By the time many owners examine their statements carefully, they discover they’re actually paying closer to 7% to 9% of their card revenue to what amounts to a silent business partner. The more successful your laundromat becomes, the more money your payment processor makes — without washing a single load of clothes.

And that’s before discussing the operational realities of the digital infrastructure.

Card systems depend on readers, connections to machines, internet connectivity, Wi-Fi stability, Bluetooth signals, cloud servers, payment processors, routers, modems, apps, firmware, and banking networks — all of which must function properly at the same time. When any part of that chain fails, the laundromat owner is left dealing with frustrated customers while waiting for technical support.

That’s a lot of dependency built into systems you don’t control.

Now, none of this means card acceptance is bad. In fact, offering debit, credit, or mobile payments absolutely makes sense for certain demographics — especially customers who carry little or no cash.

The real question is whether eliminating coins entirely is actually the smartest business decision.

Let’s examine some of the most common arguments used to sell the “coinless laundromat” concept.

1. “Coins Have to Be Collected”

True enough.

Coins don’t collect themselves. Owners have to empty coin boxes, count the money, do the bookkeeping, and maintain the change equipment. Time has value, and no experienced operator would deny that.

But card systems are not maintenance-free.

Readers go offline. Touchscreens freeze. Revalue kiosks need to be rebooted. Networks fail. Software glitches happen. CSV files have to be exported and input into different programs.

And despite what some providers imply, veteran laundromat owners rarely haul mountains of quarters to the bank. Most quarters simply go right back into the change machine and continue circulating through the store. The same coins are reused over and over again to generate revenue.

Imagine that: a payment system with no subscriptions, software licenses, or revenue-sharing agreements.

Card-system advocates also like to argue that when a change machine goes down, the store loses money.

But that usually says more about a lack of backup planning than coins themselves. Smart owners keep spare hoppers, bill acceptors, and parts on hand. Swap the part out, send the problem part to a service center for repair, and put it back on the shelf.

Besides, there’s an important distinction many people overlook:

If a coin-drop jam occurs, only one machine is affected. If the internet fails, the processor crashes, or the server goes offline, an entire store can suddenly stop accepting payments.

That’s a very different level of vulnerability.

Another way to look at it is to use the same argument that card systems use when the topic of various fees comes up. Consider coin collection part of “the cost of doing business.” Except it costs only what you’re willing to pay yourself.

2. “Coin Stores Are Targets for Theft and Vandalism.”

Unattended laundromats are targets for theft and vandalism regardless of payment type.

A card system doesn’t magically eliminate that reality.

In fact, touchscreens, protruding card readers, kiosks, and payment terminals create their own vulnerabilities. A denied transaction, a frustrated customer, a collision with a laundry cart, or an angry outburst can quickly turn expensive electronic hardware into an expensive repair or replacement bill.

Card systems may reduce certain forms of theft, but they also introduce entirely new failure points and expenses that traditional stores simply don’t have.

3. “Card Systems Increase Revenue”

This is probably the most repeated claim in the industry. And maybe it’s true in some locations.

But the question most owners are not asking: How much?

Five percent? Ten percent? More?

The answer is usually vague because every situation is different.

Let’s say a laundromat installs a $50,000 card system and experiences a 5% increase in revenue. At a $30,000 monthly store average, that amounts to roughly $1,500 in additional revenue per month before debt service and other associated fees.

That means the initial investment alone could take nearly three years to recover — and much longer if the system was financed.

Another popular talking point comes from Visa and Mastercard studies showing that customers tend to spend more when using credit cards than when using cash.

Those studies were conducted for larger retail purchases, such as furniture, vacations, food, or clothing.

But laundromats are built on microtransactions (transactions less than $25). A customer deciding whether to wash two loads or three has a different psychology from someone financing a new wardrobe.

Those studies are constantly repeated in laundromat sales presentations, yet there is very little evidence of meaningful increases in small-ticket laundry spending.

And there’s another factor many investors overlook:

Some of the best laundromat locations are in underbanked or heavily cash-based communities. If your customer base prefers cash, forcing a fully digital system into that environment may create friction instead of growth.

Convenience for the owner does not automatically mean convenience for the customer.

4. “Card Systems Provide Better Data and Analytics”

“Data” and “analytics” have become buzzwords in every industry.

And yes — information is important.

But data only has value if you understand what it means and know how to use it.

Most experienced laundromat owners already know their busiest days, peak hours, most popular machines, and customer patterns simply by operating their business well. On top of that, modern equipment manufacturers like Alliance Laundry Systems, Dexter Laundry, Continental-Girbau, and Laundrylux already provide machine-level reporting and performance data.

You don’t necessarily need a third-party payment platform taking a percentage of your revenue to see your business’s analytics.

And despite all the talk about “dynamic pricing” and penny-level flexibility, most laundromats still raise prices the same way they always have: By quarters.

The Bottom Line…

The modern card-system movement is often marketed toward new investors chasing the dream of a fully unattended, passive-income laundromat.

But laundromats are still operational businesses. They require maintenance, customer service, problem-solving, and oversight regardless of how customers pay.

The point is not that card acceptance should be ignored. In many markets, offering card and mobile payments is absolutely the right decision.

But there’s a major difference between offering only a digital payment option and completely surrendering your store to recurring fees, fragile technology chains, and third-party processors that profit from every transaction. Coin acceptance protects your profitability. It allows you to better absorb the fees associated with card acceptance.

That’s why hybrid systems make the most sense for many operators.

Let customers pay however they prefer — quarters, debit cards, credit cards, or mobile apps. Meet the customer where they are without abandoning the reliability and profitability of coin acceptance.

The future isn’t coin-only.

It isn’t card-only either.

The future is flexibility.

Give customers the choice to pay how they want — while keeping control of your own business.

For over 70 years, Standard Change-Makers has been designing and manufacturing currency change machines with the needs of self-service businesses in mind. Since 1955, we’ve worked alongside laundromat owners across the U.S. and Canada — including the 86% of vended laundries that still rely on coin acceptance as a primary payment method.

We understand that every store and customer base is different. Whether you’re considering coin, card, or a hybrid payment model, our goal is simple: help owners make informed decisions based on long-term reliability, profitability, and what works best for their customers — not just the latest sales pitch.